“If Glu doesn’t hit $12, I’ll eat my shirt… and on streaming video, too,” exclaimed Jason Bond of JasonBondPicks.com. “Cowen’s latest projection intimates a gross profit of approximately $67 million – maybe more, yet the stock trades at a forward P/E of 6.8? The S&P trades at 19.3, and where’s the EPS growth coming from over there – from stock buybacks?! That cannot go on forever.”

Bond goes on to say that, even with guidance of a drop in gross margin of 58%, the company’s operating income could potentially reach more than $100 million by the close of fiscal 2015. And at that rate, Glu’s income tax liability could actually rival the company’s 2013 quarterly revenue prints. See previous article, titled, GLUU: Up 61.7% From Our May 15 ALERT; Stock Still A Potential 2-Bagger.

“Which would you want, the S&P at a P/E of 19.3, or GLUU, today, at a projected 6.8?” Bond asked rhetorically.

Cowen & Co. Projects $200 Million-Plus – Atop Today’s Revenue!

The out-of-the-blue sensation of Kim Kardashian: Hollywood has turned the media spotlight onto Glu Mobile (GLUU), especially after King Entertainment’s (KING) stunning fall from grace and Zynga’s (ZNGA) stalled turnaround story.

Before we delineate the compelling reasons for the rather provocative title of this article, first refer to Jason Bond’s call on GLUU, back on May 15 (KING, ZNGA & GLUU: Which One Best For Investors?), and the subsequent updates to GLUU’s remarkable progress and share price appreciation.

“[Glu Mobile] has all the makings of a takeover candidate,” Bond stated in his May 15 aticle. “Since the mobile gaming market offers a high gross margin and an eye-popping market growth profile, Glu’s continued excellent performance could be attractive” to suitors wanting buy Glu’s talent and revenue stream.

However, back in May, no one knew what would happen to Glu Mobile next.

The bombshell success of Kim Kardashian: Hollywood (KK) and subsequent large revision hike to revenue – issued by Cowen & Co. – will most likely drastically change Glu’s bottom line to one of significant profit.

According to Bloomberg News of Jul. 10, “Annual revenue from Kim Kardashian: Hollywood may reach $200 million, estimates Douglas Creutz, an analyst with Cowen & Co. in New York, who has the equivalent of a buy rating on Glu Mobile and expects the stock to rise to $6 in the next year.”

Nearly a month later, nothing has changed to alter Cowen’s forecast.

“This is our biggest casual game ever,” Glu Mobile CEO Niccolo De Masi told Bloomberg West on Aug. 8. “This is probably going to be our biggest game of the year.”

So, more than six weeks later, KK has reached as high as the no. 3 top-grossing game in the U.S., eliminating speculation that KK is merely a ‘flash in the pan’.

The statistics are in, and the trend is clear. “I think the game [KK] will go a long time,” De Masi asserted.

In fact, De Masi & company think Glu has hit onto something much bigger than just a top-grossing game; he told Bloomberg that the success of KK suggests that Glu may have “defined a new genre” and that the company is actively exploring additional opportunities with other celebrities with similar fan bases.

Glu Mobile is No KING.

In addition to KK’s overnight hit, Glu’s bullpen of money-makers provides the mobile games maker with a much more stable revenue base from which to grow, of which Zynga and, most recently, King have failed to convince Wall Street.

In addition to the 11 games indicated in the pie chart, below, Glu has just released nine more games in beta, including Amazing Battle Creatures; Bingo Flick 3D; Casino World; Cannon King; Contract Killer 3; Racing Empires; Royal Horse Racing; Tap Sports Baseball; Westward Journey.

And with revenue from Diner Dash and Racing Rivals coming online from the Cie Games acquisition, announced on Jun. 30, Glu has clearly overcome the ‘One-Hit Wonder’ syndrome which had once been an issue with Zynga, but now plagues King Entertainment.

King Entertainment has demonstrated how vulnerable the company’s revenue truly is. Fears of the One-Hit Wonder syndrome during King’s March IPO have been realized, as predicted by not only Jason Bond, but all of Wall Street, as the IPO price of $22.50 was sold and has since never recovered.

With so much of King’s total sales dependent upon its sole one-hit game Candy Crush Saga, it was only a matter of time when the company would guide lower and trigger a panic rush out of the stock.

On Aug. 13, KING opened nearly 25% lower, after the company reported a drop of $30 million, or 5%, in second-quarter bookings. Candy Crush Saga’s slumping revenue was the primary culprit for the overall drop in bookings for the quarter, according to the company.

Guidance was worse. King now expects current-quarter bookings to drop another 14% to 18%.

Contrastingly, Glu offers investors more stable revenue streams and a better chance of profiting from the explosive growth rate expected for this space. Why add so much company risk to a space expected to grow at 27.3% CAGR through 2016?

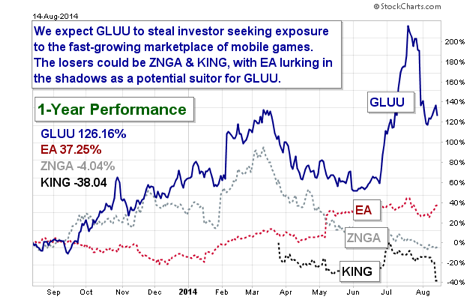

Compare and Contrast GLUU, ZNGA, KING and EA

The following chart, below, reveals GLUU’s relative performance against Zynga, King Entertainment and Electronic Arts (EA). Though we don’t regard Electronic Arts a direct competitor to GLUU, we do feel, however, that EA could be mulling over the possibility of buying GLUU for its exposure to the mobile games market, executive talent and exploding revenue streams.

We are thinking along the lines of a potential takeover of Glu Mobile due to the rapid company’s rapid top-line growth rate, coupled with EA’s need to deploy a portion of its $2.3 billion of cash/cash equivalents. At $458 million, Glu Mobile is attractively priced right now, in our opinion. Before the company reports earnings in the coming quarters, Electronic Arts or, maybe, Amazon should act now.

Jason Bond’s Final Thoughts

“In June, we saw GLUU decouple from ZYGA and KING. More and more investors of the mobile games space have been jumping the Zynga and King boats and landing on GLUU,” Bond concluded. “Glu was first to Google Glass and Amazon Fire TV; its aggressive in China and elsewhere. Now Glu’s execs are first to exploit the celebrity angle.

“At the moment, this company is firing on all cylinders. We remain long, and will reappraise the stock again at $12.”

Disclosure: I am long GLUU

Consensus estimate for 2015 eps is $0.24. That amounts to a forward P/E of 21.6. Where do you get 6.8?

The forward P/E was estimated from Cowen’s $200 million revenue from KK. It’s our forward P/E estimate based on Cowen. Analysts have not adjusted for the KK revenue yet. If Cowen is right, all revenue projections from analysts are out the window.

http://www.jasonbondpicks.com/blog-posts/gluu-up-61-7-from-our-may-15-alert-stock-still-a-potential-2-bagger/

The article above has a P/L that includes KK’s revenue. It’s rough, but anything close to $200 million by this time next year will blow the top off analysts’ estimates.

How much longer do you forsee GLUU downtrending?

Hard to know that for sure but my best guess is it rounds out and turns up soon pushing low $6’s before it consolidates.

How old is this interesting analysis? I’m long too.

I just wrote it a few days ago.

Let me elaborate more. Without KK, the $160 million revenue projection is the mean analyst estimate. During the first half of the year, GLUU has already booked $85 million, so the $160 million the fiscal year is not going out on a limb.

However, with KK, net income should rise rapidly even from a lower gross margin. GLUU has no debt. Even at the lower margin rate, an extra $200 million to the top line should easily cover the present rate of R&D and SG&A ($30 million per quarter) for some quarters to come.

We agree; the stock’s $6 resistance could become support in the coming quarters. We will know soon whether Cowen’s estimate for KK is sound, but we don’t foresee anything that’s obvious to disrupt our analysis enough to reconsider our positive sentiment on GLUU.

There seems to be a signature to the trend and duration of most games which become revenue blockbusters. Cowen noted the similarity of the data between KK and other big hits.

why we cant see the date for post or comments ???

Interested in what time scale your $12 eat-my-shirt challenge is over