Good evening,

Stocks traded once again to record closes this week, with the DJIA, S&P500, NASDAQ, DJTA and Russell 2000 closing ‘in the green’ and with momentum.

It appears President Donald Trump has done it again. Trump’s promise to deliver a “phenomenal” tax plan to Congress juiced stock buying and short covering across the board. He even cheered of the “confidence and optimism” his plan has generated, “even before the tax plan rollout!” he tweeted.

The NASDAQ finished the week with a seven-day streak of record-high closes, matching a seven-day streak in 1999. As a group of indexes, this week’s five-day streak of record closes in the DJIA, S&P500 and NASDAQ hasn’t been achieved since 1992.

But, the most bizarre statistic, in my opinion, is the three-month streak in the major averages not closing at a 1% loss on any given trading day since October 11.

And of course, many times I’ve mentioned the streak of crazy VIX prints below 11. Frankly, I’ve never remembered a market such as this one. But, as long as the DJIA and DJTA confirm a Dow Theory ‘buy’ signal, I expect higher stock prices.

However, I want to be clear, very clear about the valuation level of this market. At the close of Friday’s trade, the S&P500 has reached a Shiller p/e of 29.14. That’s the third-highest reading for the Shiller p/e ever! In 1929, the Shiller p/e calculated to 30.08, and the tech stock bubble pop of January 2000 began with a Shiller p/e of 44.19. The rapid stock market bear market of 2008 began with a Shiller p/e of 27. With earnings estimates notching down, a market that’s rising while earnings are flattening is a recipe for trouble.

A data set of hundred years of daily statistics reveal a Shiller p/e above 27.6 falls outside the 95% confidence level (2 standard deviations) of daily p/e ratios. I think the point has been made.

However, with central banks alternately creating more credit (money) ‘out of thin air’ at increasing rates, previous hyperinflationary periods have almost always included higher stock prices along the way. Much work has been done to measure asset values in Germany during the post-WWI era (1921-1924) of hyperinflation. Even though the Reichsbank slowly, then quickly, replaced falling GDP by expanding the money supply of marks, the stock market continued to rise.

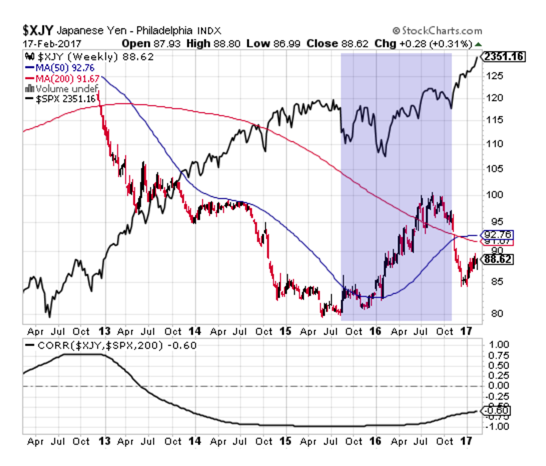

Today, the issue of money supply creation by central banks is much different in execution from the Reichsbank in the early 1920’s in that, the ease of cross-border trading allows easy monetary policy in Japan to translate to higher stock prices in US markets, for example. And that’s what has happened to global capital flows since the summer of 2014, as newly created yen, which found no opportunities for a return on capital expenditures in Japan enterprises, made its way into dollar-denominated investments in a game of arbitrage of selling zero-rate securities from the BOJ and buying positive rates in the US Treasury 10-year notes and blue-chip, dividend-paying stocks.

From the chart, below, notice the fall of the yen against the US dollar running concurrently with rising US stock prices. Pay particular attention to the rising yen off the August/September 2015 low and up to the time leading to the US election on November 8. It appears without help from the BOJ, US stocks struggle. In fact, I’m surprised US stocks didn’t suffer a greater selloff during the time period between August/September 2015 and February 2016.

Remember what I was saying during those bleak days? “Patience.” And it paid off from my long position and big score in FNMA!

As I see today’s stock market action, the four central banks that make up more than 90% of all central bank reserves have collectively and alternately debased their respective currencies at increasing rates since 2008, with the numerous QE operations from these four banks elevating stocks and bonds prices. If this situation continues, it’s good for stocks, and has been the primary reason to stay long US stocks throughout most of this eight-year rally, as prescribed by Dow Theory. Although today’s S&P 500 Shiller p/e has nearly reached the p/e level prior to the stock market crash of 1929, more ‘money printing’ can take stocks even higher as Weimar has shown.

Okay, now here’s where this money printing business gets tricky. Central banks were rudely awaken to the limits of their ways at the start of 2016. When Japanese rates went negative on the Japanese 10-year yield during the first quarter of 2016, bad things began to happen in the eurodollar market (i.e. US dollars held overseas and outside the Federal Reserve system), and as a result, smart money rushed into the US dollar and gold market.

Do you remember the rally in the dollar-gold price and huge rally in gold stocks at that time? And do you remember the crashing yields on the US Treasury 10-year note? So, we know where money will flow during the next crisis: US dollar and gold.

The bottom line take-away from the near-collapse of the global financial system in the first half of 2016 is: interest rates most likely have bottomed. I believe DoubleLine Capital founder, Jeffrey Gundlach, is correct when he told CNBC on September 8 that “[interest] rates have bottomed and have begun to rise on a secular basis.”

Therefore, the course of ever increasing injection of credit (currency) into the global financial system by the Japanese to support global asset prices is probably over. Ditto for German sovereign obligations; German 10-year sovereign paper briefly traded below zero percent as well, resulting in a poor auction results for the mighty bunds soon after. Although not leading as headlines in the financial press, the US dollar has been shown to be poised as the last man standing during a crisis, and that central banks have become powerless and irrelevant to what happens next.

To my way of thinking, if Gundlach is correct (as I believe he is), the only hope left for the global economy is a revitalization of real US GDP. Isn’t that what the Trump campaign was all about? Bringing back American jobs? Sure. But here’s the problem that even the grandest of chess grandmasters can’t solve, which is: how can a revitalized US economy and, by implication, a rising US dollar coexist in a global economy dependent upon a plentiful supply of eurodollars? Theoretically, according to Triffin’s paradox, this cannot happen! And has never happened. That’s what bothers me.

In other words, if Donald Trump wants to repatriate US dollars stuck in overseas banks, wouldn’t the eurodollar market become more tight? Therefore, all else being equal, any financial crisis will again come from overseas and the Fed, ECB, BOJ and BOE won’t be able to use the same ‘policy tools’ to cope with a flight out of emerging market currencies. I ask, how would Bank Negara (Malaysian central bank) stem a currency flight out of the ringgit? Or in Thailand? In Brazil? And so on. Global central banks don’t hold enough reserves as it is now.

So now what? I suggest that until Dow Theory give us a ‘sell’ signal, remaining long in stocks is the ‘textbook’ choice at the moment. However, as soon as the Trump euphoria turns to a rational discussion of the realities of macro-economics as I’ve outlined, global stock prices may come under pressure, leaving the US dollar and gold as the only repositories of safety. As the eurodollar becomes that more scarce, a potential for rolling emerging market currency crises increase. Then, who knows what happens?

For my subscribers who wonder what to do with retirement capital not designated as ‘play’ money, famed Swiss money manager, Marc Faber, has frequently suggested that investors who seek balance between their stock holdings and other asset classes should own at least 30% of their total portfolio value in gold bullion as a currency. Has anyone noticed Jeff Gundlach bought some gold bullion in early 2016 to increase his ‘cash’ position? More aggressive traders have been buying the GDX and GDXJ. Look at their charts.

I’ll close the first half of the Long-Term Weekly report with an excerpt from my colleague and friend, Jeff Williams, at PennyPro Weekly, who expresses my sentiments exactly regarding an issue that he and I have been talking about for some weeks, which is, the French election of April 23 and, most likely, the runoff and final election on May 7.

Following our latest talk, Jeff agreed to publish our mutual thoughts in PennyPro, and allow me to include the excerpt in my newsletter. Jeff penned:

WHAT COULD HAPPEN?

A ‘Black Swan’ event, as we’ve mentioned before can at anytime instantly create a no-bid market following this nearly nine-year rally. We recommend to remain hedged with a goodly amount of gold bullion during the ongoing Obama-Trump reflation of asset prices.

Unlike the fall in the dollar-gold price in the 2008-9 meltdown, we highly suspect that if another meltdown in stocks did occur, it would most likely trigger a dollar-gold price to soar, instead, as traders have conditioned themselves for a stock rout throughout the rally that began in March 2008. So, keep all of this in mind at all times, as we see more and more well-known hedge fund managers disclosing gold bullion purchases.

And speaking of swans, let’s revisit the ‘Gray Swan’ possibly coming out of Europe with the French elections scheduled for April 23. After reading a CNBC report about the results of an Artificial Intelligence (“AI”) program regarding the French presidential election, we think we should add to our do-list a more frequent search for the latest french presidential race polling data. If you remember, the engineers behind the AI program discussed in the CNBC article is the same group that predicted a ‘Brexit’ and Trump win. AI predicts a Le Pen win. Oh my.

Populist candidate for the French presidency, Marine Le Pen (National Front President), who leads in the polls, has some traders fearing of a growing possibility of financial crisis stemming from the French election. As many of you may already know, Le Pen is the French version of Donald Trump. A Le Pen win will be the trigger for the “beginning of the end” of the euro, according to Arun Kant, CEO of Singapore-based Leonie Hill Capital, the financial firm that incorporates AI technologies to the company’s forecasts.

CNBC stated, Kant “incorporates inputs such as social and traditional media discussions, polling, economics and demographics — predicts that Le Pen will ‘walk over’ her opponents in the first electoral test and then prove most forecasters wrong and steal the lead in the second ballot.”

The AI model predicts a close race with challenger and former-French Minister of the Economy, Finance and Industry, Emmanuel Macron, 39-years old, in the May 7 runoff.

And what if Le Pen wins on May 7? “[A Le Pen win] may lead to a financial crisis much sooner than anyone thinks,” Kant concluded.

Okay, so I’ve just suggested that a financial crisis would most likely come from overseas. Right? Now we have a controversial election between the established order in France with their candidate, Macron, whose party has been taking marching orders from Brussels for years, running against the presidential-race leader Marine Le Pen, a Trump-like political figure in France. Could a Len Pen victory suddenly create a vicious demand for the US dollar, and at a time of a growing eurodollar shortage? You bet it could!

Remember how I started the year with a forecast of a stronger US dollar and a strong dollar-gold price? Well, now you may understand my thinking on what appears to be a contradiction of a higher dollar-gold price and a strong US dollar.

My baseline still is for Le Pen to lose the presidency, but apparently this AI stuff is a lot smarter than I am. I have to admit I was surprised at ‘Brexit’ and equally surprised by the significant electoral winning margin of Trump’s presidential victory. AI picked up on both ‘unlikely’ political events. Now it predicts a Le Pen win. Hmm.

Okay, let’s talk about the stocks I’m watching now.

This Week’s JBP Stock Ideas

My current portfolio: LQMT, CROX, KNDI and TWTR calls

On February 14, I added 5,000 shares at $4.24 to my KNDI holdings; it’s finally starting to show signs of a reversal.

I sold half my GRPN at $3.57 for a $200 score. Holding 10,000 shares had become too much with SIEN, WTW and LC in my cross hairs.

And I have a good-til-canceled (GTC) order to buy 1,000 shares of WTW at $12.40, and angling to buy 1,000 shares of SIEN into the next dip (and it ain’t dipping yet). Although there was no company-specific news, the pharmaceutical ETFs were ‘on a tear’ this week, taking SIEN higher in sympathy with the sector.

LC has gotten away from us a little, but I like the stock at higher lows, so we’ll watch for if the stock settles above its support trend line.

To by brutally frank, I was surprised at LC’s operating income during Q4, but haven’t been shaken from my expectation of the company turning the business around; it’s just not going to happen as quickly as I once hoped.

On February 15, I alerted I took my remaining GRPN off the table for a 7% ($1,000-plus) score, for a total profit of $1,200. Earnings were good, as I expected. I was patient with the stock, and my patience was rewarded.

Let’s get to my Watch List: LendingClub (LC), Sientra (SIEN) and Weight Watchers (WTW).

LENDINGCLUB (LC)

The company has been in a turnaround phase following revelations in May 2016 that Lending Club CEO, Renaud Leplanche, had sold $22 million of loans to a investment bank, Jefferies, that did not match the client’s requirements, i.e., fraud. On May 16, the U.S. Department of Justice served a subpoena for records involving the company’s dealings with Jefferies.

As a result of the terrible publicity surrounding the questionable ethics of the company’s CEO, LC had lost nearly 57% of market capitalization due to the scandal, but has since recovered much of the initial drop, rallying back.

But this ‘turnaround’ stock may be just beginning.

The company has regained confidence among its credit suppliers in the banking industry as a result of LendingClub improved internal controls, a new CEO, and continued leadership in this new industry segment.

Competitive forces have entered the mix for LendingClub. As peer-to-peer gains traction in the Internet lending space, many of the company’s competitors will most likely drop off from the race in this new and exciting form of lending. LendingClub, however, shines in this environment, as the company’s seeks to consolidate business left behind by fallen competitors.

Traders of LendingClub were delighted with news in late 2016 that National Bank of Canada awarded open credit lines with the company in the amount of $1.3 billion. This award signals the end of LendingClub’s fall from grace, impelling Jeff to highly recommend LC as a potential huge play in the exciting alternative lending space.

On February 14, LC reported Q4 earnings, and the picture was not as good as I expected. Sure, I was much closer with my estimate of $126.4 million of revenue for the quarter than the mean analyst estimate of $121.93 million (actual: $129 million), but everyone was baffled at the 25% y-o-y increase in operating expenses.

So what to do? As I stated in my confidence in LC in its turnaround efforts hasn’t waned. However, at what price I’d like pick up some LC shares for a shot at a better-than-expected 2017Q1 earnings report is the $64,000 question. I’ll let you know when I know.

ABOUT LENDINGCLUB (LC)

LendingClub Corporation, together with its subsidiaries, operates as an online marketplace that connects borrowers and investors in the United States. Its marketplace facilitates various types of loan products for consumers and small businesses, including unsecured personal loans, super prime consumer loans, unsecured education and patient finance loans, and unsecured small business loans. The company also offers investors an opportunity to invest in a range of loans based on term and credit characteristics. It serves investors, such as retail investors, high-net-worth individuals and family offices, banks and finance companies, insurance companies, hedge funds, foundations, pension plans, and university endowments. LendingClub Corporation was founded in 2006 and is headquartered in San Francisco, California.

SIENTRA (SIEN)

Sientra (SIEN), a maker of silicone breast implants and a budding successful turnaround story from an unfortunate factory stoppage at its third-party manufacturing facility in Brazil, Silimed Industria de Implantes Ltd. A little more than a year ago, due to a European regulatory agency issuing a marketing suspension of all products made at the Brazil plant, after flaws were found in some silicone implant products made at the facility, trouble came to Sientra, but through no fault of theirs.

Although Sientra manufactured implants at the plant employed production standards approved by the US FDA, and were independent of other processes at the facility, Sientra voluntarily suspended operations in September 2015 until a third-party inspector verified Sientra’s implants were not among those produced by the methods of other Silimed customers exporting to the European market.

Following the news of Sientra’s voluntary production suspension, the share price of SIEN crashed to as low as $3.34 by mid-November, from a high of $26.67 reached in late-June.

As a result of the work stoppage, Sientra’s revenue plummeted in Q1, Q2, Q3 of this year to a fraction of the company’s Q3 2015 peak sales performance. But since the stock’s November low, SIEN is coming back steadily following an announcement in early-February 2016 that stated the Brazilian plant is again operating and shipping product.

Previous customers who suspended orders to Sientra are coming back to the company, who, at the height of Q3 2015, supplied between 7% and 12% of all implants to a US market, with estimates ranging from $200 million and $300 million per year of revenue, and growing.

On December 5, 2016, SIEN soared to as high as $10.22 (27.6%), following a news release by the company of an FDA pre-market supplement (PSA) approval for the company’s four new implant styles and shapes. These new products will be added to its present line of nine offerings. The company expects to begin delivery of the four new implant in Q4 2017.

My take: I like the stock for its hidden future trend of higher revenue, as the results of a survey conducted by the company of the customers affected by the work stoppage at the Brazilian plant indicated that nearly all customers expect to order Sientra products again when they become available.

And there is a good reason for this nearly-perfect positive response.

First, Sientra is the only company of the three operating in the US (the other two: Mentor, Natrelle) who offers a two-year guarantee against ‘capsule contracture’, an issue of primary concern of most patients and surgeons. Sientra’s rate of contracture is, indeed, the lowest of the three makers. And the company also hold the distinction of offering implants with the lowest in incidents of rupture.

This is a big deal, as far as I’m concerned. Imagine if you were undergoing an implant procedure. Wouldn’t you want an implant with the highest reputation of product safety? Of course, you would.

Second, patients report that Sientra implants feel more natural, which is definitely another big win for Sientra.

In short, Sientra’s implants are best of breed, which weighed heavily on my decision to engage this stock. I expect revenue to regain the $10 million-plus per-quarter level.

Read Sientra’s Quick Fact Sheet

ABOUT SIENTRA

Sientra, Inc., a medical aesthetics company, develops and sells medical aesthetics products to plastic surgeons and patients in the United States. The company offers a portfolio of silicone gel breast implants for use in breast augmentation and breast reconstruction procedures; and breast tissue expanders. It also provides body contouring and other implants, including gluteal, pectoral, calf, facial, nasal and other reconstructive implants. Sientra, Inc. was incorporated in 2003 and is headquartered in Santa Barbara, California.

Source: Finviz.com

WEIGHT WATCHERS (WTW)

I’ve add WTW as another turnaround stock with potential of surprising investors. And with 18.6 million shares sold short and only 27.39 million shares floating, the risk of a massive short squeeze may be unlike any other stock I’ve featured in these reports.

The company’s earnings report is due on February 28, after the bell. The Q4 consensus earnings per share is $0.18 per share on revenue of $271.4 million. I’m expecting $0.20 per share on revenue $274 million. If my estimate is closer to the actual result, how high can this stock go with two-thirds of the stock’s float held short? There’s no doubt, the risk lie with the shorts.

The added factor to WTW is the cache the company inherits from Oprah Winfrey, who, according to a October 2015 13D filing with the SEC, holds 10% of WTW, with an option to buy another 5% of the company’s shares.

In short, I think the worst is behind WTW. And if I’m correct, the rally that can come from a good portion of the 18.6 million shares covering will be a sight to see. If you’re short this stock, be careful, because too many traders are on one side of this boat.

And don’t think Oprah Winfrey won’t be defending her approximately $40 million investment in the company. Do a Google News search with the search term, “Oprah Winfrey Weight Watchers” and the parameter of retrieving articles of the past week. You should find eight. At any time, Oprah could protect her investment by skillfully ‘plugging’ Weight Watchers on any given day.

ABOUT WEIGHT WATCHERS (WTW)

Weight Watchers International, Inc. provides weight management services worldwide. The company operates in four segments: North America, United Kingdom, Continental Europe, and Other. It offers a range of products and services comprising nutritional, exercise, behavioral, and lifestyle tools and approaches. The company also engages in the meetings business, which presents weight management programs, as well as allows members to support each other by sharing their experiences with other people experiencing similar weight management challenges. Weight Watchers International, Inc. was founded in 1961 and is headquartered in New York, New York.

Until next time…

Trade Wise and Green!

Jason Bond

0 Comments